Accrued revenue, also known as unbilled income, is the revenue a company earns but hasn’t yet invoiced or received payment for.

What is accrued or unbilled revenue?

Accrued revenue is income a company has earned but hasn’t received yet—often because the customer hasn’t been invoiced or still needs to pay.

According to Generally Accepted Accounting Principles (GAAP) and International Financial Reporting Standards (IFRS), businesses must record income and expenses when they’re earned, not necessarily when they’re paid.

This is especially important for service-based organizations and subscription-based models, where payments often come in after services are delivered. Tracking accrued revenue helps finance teams monitor income in real time, offering a clearer picture of the company’s financial health—even before the money hits the bank.

<<Download the SaaS metrics cheat sheet.>>

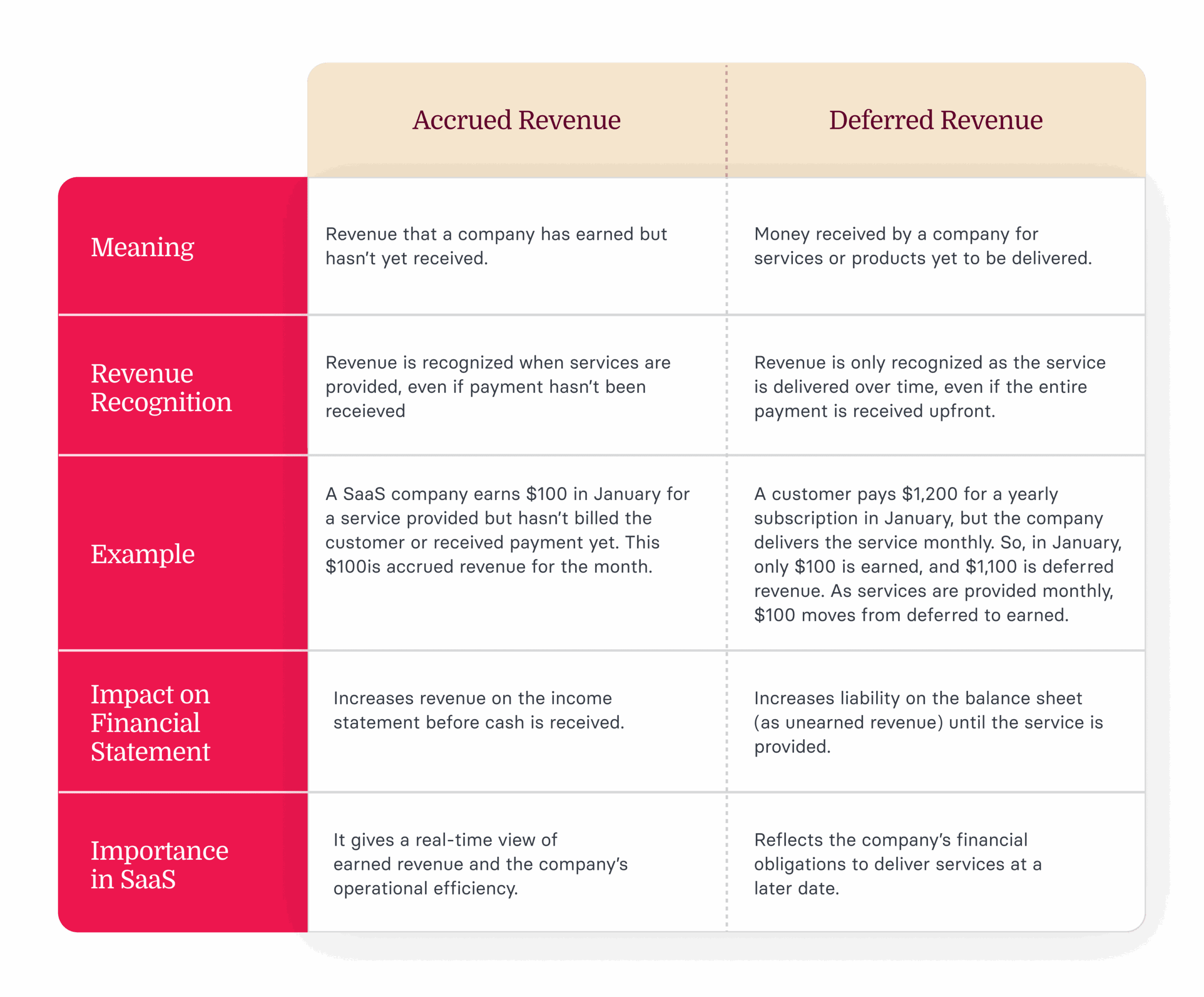

Accrued revenue vs. deferred revenue

Accrued revenue isn’t the same as deferred—or unearned—revenue. While they’re related, each metric serves a different purpose. Both follow Generally Accepted Accounting Principles (GAAP), which require businesses to recognize revenue when services are delivered—not when payment is received.

Let’s start with accrued revenue. Put simply, it’s income your company has earned but hasn’t received yet—often because the customer hasn’t been invoiced or hasn’t paid. For companies with subscription-based business models, accrued revenue is a key financial metric.

Tracking accrued revenue shows how much income you’ve actually earned during a given period. It offers real-time insights into your financial health and operational efficiency. By recognizing revenue as services are delivered—rather than when payments arrive—you get a more accurate view of performance.

Deferred revenue, on the other hand, is income you haven’t earned yet. It reflects payments you’ve received in advance for services not yet delivered. In subscription-based models, even if a customer pays upfront for several months or a year, only the portion tied to completed service is recognized as revenue. The rest remains deferred until earned.

Examples of accrued or unbilled revenue in real-world scenarios

To better understand how accrued revenue works, let’s look at a couple of hypothetical examples.

Company A offers advertising services and charges clients based on the number of ad impressions delivered. Clients are billed monthly, at the start of the following month. In January, Company A delivers 2 million impressions for a client, at a rate of $5 per thousand impressions. That amounts to $10,000 in accrued revenue for January—even though the client won’t be invoiced or pay until February.

Now consider Company B, which is managing a long-term project. According to the contract, billing happens at specific project milestones—not on a fixed schedule. By the end of January, Company B completes work worth $15,000, but can’t bill until early February. Still, it records $15,000 in accrued revenue for January, reflecting the value of the services provided.

In both cases, there’s a lag between service delivery, billing, and payment. That gap is where accrued revenue shows up—offering a more accurate view of what’s been earned.

How to calculate and record accrued (unbilled) revenue

Calculating accrued revenue is straightforward. Add up the income from all customers who’ve received services during a specific period but haven’t been billed yet. That total is your accrued revenue for the period.

When calculating or recording accrued revenue, keep a few key points in mind:

- Subscription contracts often run for months—or even years—so it’s important to track and recognize revenue consistently, based on when the service is actually delivered

- If a free trial transitions into a paid subscription without a break, you’ll need to reflect that shift in your accounting records to accurately mark the start of the paid service

Below is a quick guide on how to record accrued revenue in line with the matching principle outlined by GAAP.

Make your chart of accounts as clean as possible with this best practices template.

Guidelines for accrued revenue journal entries

In accrual accounting, accurately recording journal entries for accrued revenue is key to presenting a true picture of your company’s financial health. By following GAAP’s revenue recognition principle—recognizing income when it’s earned, not when it’s paid—you give stakeholders a clear and reliable view of performance.

Recording accrued revenue is fairly straightforward if you’re familiar with double-entry bookkeeping and basic accounting concepts like trial balance, balance sheets, or accrued income statements.

At a high level, there are two main steps:

- First, record the accrued revenue as it’s earned—even before payment comes in

- Then, adjust those entries after you invoice and receive payment, transitioning the amounts from accrued revenue to accounts receivable, and eventually to cash

When logging accrued revenue, you’ll typically debit an “accrued revenue” account and credit a revenue account. This boosts both your assets and your recorded earnings for the period.

Once you invoice the customer but haven’t yet received payment, the entry becomes “accounts receivable.” After the payment is received, you update the records again—this time turning the receivable into cash. That final step affects the balance sheet, but not the income statement.

The role of accrued revenue in financial analysis

Accurately managing accrued revenue is essential for producing reliable financial statements—a core need for finance teams, since data drives all strategic decisions.

Tracking accrued revenue helps you assess your cash flow, forecast future revenue, and make smarter investment or budgeting choices. It also ensures your revenue recognition stays aligned with service delivery—giving you a clearer view of profitability and operational efficiency.

Most importantly, it supports transparency with stakeholders, highlights your company’s growth potential, and helps ensure compliance with accounting standards. All of this makes accrued revenue a critical piece of financial analysis and long-term planning.

Navigating accrued revenue challenges in SaaS

Managing accrued revenue can be complex—especially in SaaS, where subscription-based models add another layer of difficulty.

Subscription contracts often create complications for revenue recognition, making it harder to accurately track and report revenue in line with accounting standards. Without the right tools, managing these processes manually can lead to inconsistencies and errors—despite the time and effort involved.

Understanding the timing of cash inflows from accrued revenue is also essential for effective cash flow management. But given the nature of SaaS billing cycles, this timing can be unpredictable.

Compliance is another challenge. As accounting standards evolve, staying compliant requires accurate and timely financial reporting. That means finance teams need clear visibility into revenue data and dependable systems to support their workflows.

To meet these demands, many finance teams turn to financial software tools that support more accurate tracking, automation, and forecasting—helping improve both compliance and decision-making.

Key takeaways

- Accrued revenue, also known as unbilled income, is the revenue a company earns but hasn’t yet invoiced or received payment for

- It is crucial for service and SaaS businesses to track accrued revenue to gain real-time insights into financial health and operational efficiency

- Accurate management of accrued revenue enhances financial reporting, compliance with accounting standards, and stakeholder transparency

- SaaS companies face unique challenges with accrued revenue due to subscription models, but robust financial planning and analysis software can streamline processes

- Regular reconciliation of accrued revenue accounts and using solid software solutions can minimize errors and optimize financial operations

Tips for managing accrued revenue effectively

To get a clear picture of your accrued revenue and manage it well, here are a few helpful practices:

- Use reliable financial software—especially one designed for subscription-based or service-driven business models. Look for tools that can automate revenue tracking, reduce manual errors, and save time.

- Reconcile accrued revenue accounts regularly with actual payments. This helps you quickly spot discrepancies and ensure your financial statements reflect your company’s true position.

- Analyze accrued revenue trends frequently. Doing so can surface insights into business performance and support smarter, more strategic decision-making.

- Review your financial statements consistently to ensure revenue is being properly recorded and recognized.

Ultimately, a dependable financial planning and analysis (FP&A) process plays a critical role in managing accrued revenue—and building a strong foundation for long-term growth.

Accrued / unbilled revenue FAQs

What is the difference between accounts receivable and accrued revenue?

Accrued revenue is earned income for services or products that haven’t been invoiced yet. Accounts receivable refers to money owed for services or products that have already been invoiced but not yet paid. The key difference is whether an invoice has been sent.

How does accrued revenue impact cash flow?

Accrued revenue doesn’t immediately affect cash flow, since no cash has been received. It represents future income and only impacts cash flow once payment is collected.

Recommended For Further Reading

Can accrued revenue be considered an asset?

Yes. Accrued revenue is recorded as a current asset on the balance sheet because it reflects money owed for work that’s already been done.

What is unbilled revenue?

Unbilled revenue is another term for accrued revenue. It’s revenue that a company has earned but has not yet received.